The Rise of OpenUSD: A Structural Challenge to the Stablecoin Issuer Model

The stablecoin landscape is facing a potential paradigm shift following the launch of OpenUSD (OUSD), a new stablecoin backed 1:1 by U.S. dollar reserves. Unlike traditional models where reserve interest income is captured primarily by the issuer, OUSD operates through a consortium of over 140 financial institutions and payment companies, including major players like Stripe, BlackRock, and Coinbase. This structure allows for the redistribution of reserve yields directly to the network of corporate partners, marking a departure from the centralized revenue models employed by established stablecoin providers.

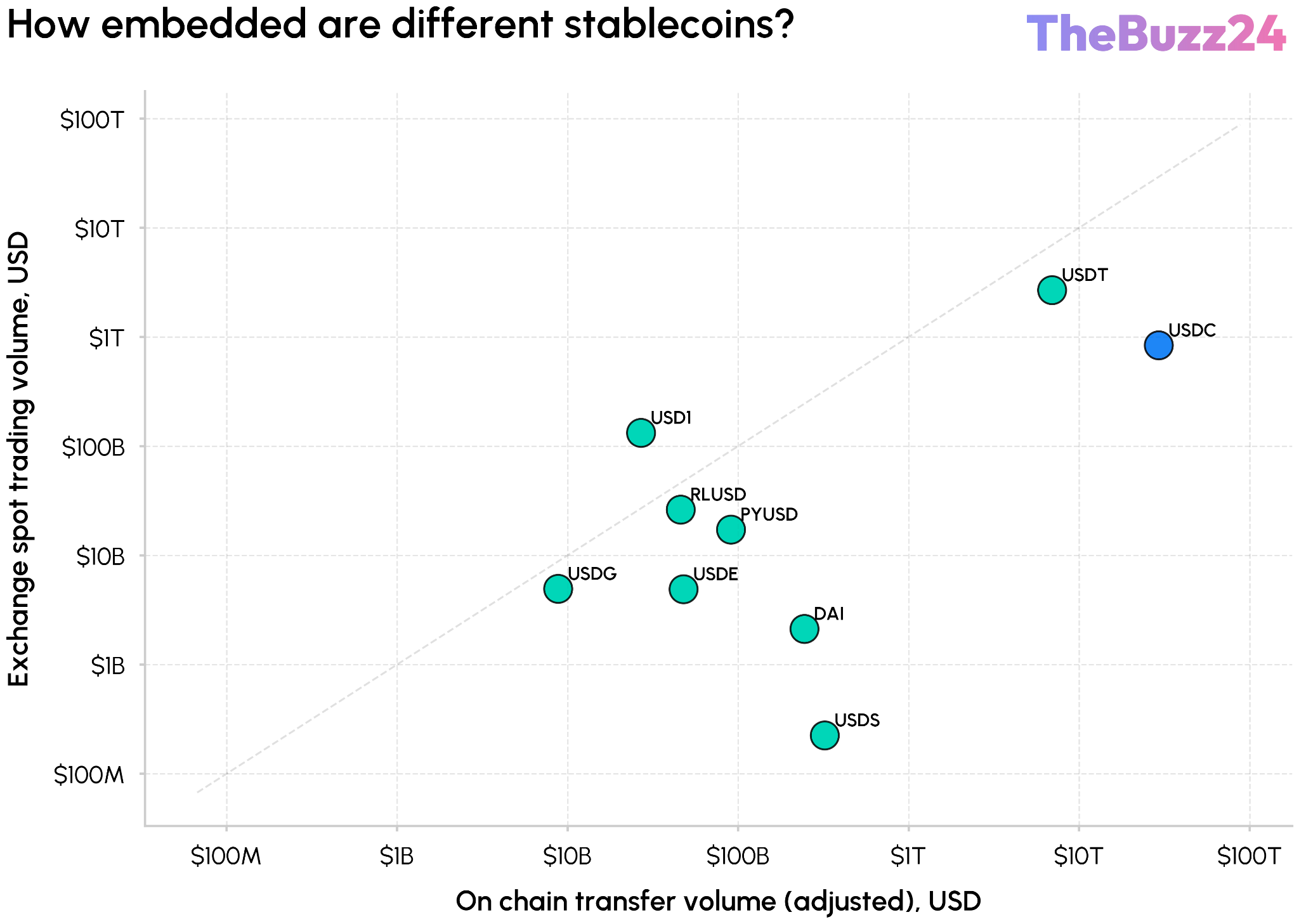

The announcement of OUSD triggered immediate market volatility, notably impacting the equity valuation of Circle, the issuer of USDC. While the market reaction suggests concerns over future profit margins, the long-term viability of OUSD depends on its ability to compete with the deeply entrenched network effects of existing stablecoins. USDC currently maintains a dominant position in the ecosystem, settling approximately 79% of on-chain transfer volume and serving as a critical liquidity anchor for decentralized finance (DeFi) protocols and major trading venues.

Circle’s competitive advantage remains rooted in its regulatory standing and its deep integration into the financial infrastructure. By securing federal oversight through the Circle National Trust, the company has solidified its position as a trusted dollar rail. Furthermore, USDC’s widespread adoption across both centralized and decentralized exchanges creates a high-velocity environment that is difficult for new entrants to replicate. While OUSD introduces a compelling economic model for distributors, it must overcome the significant liquidity moats and regulatory trust that currently sustain the dominance of established stablecoins.

Key Takeaways

- OpenUSD introduces a consortium-based model that redistributes reserve interest income to network partners rather than a single issuer.

- USDC maintains a dominant market position, settling nearly 80% of on-chain transfer volume and serving as a primary liquidity source for DeFi.

- The competition between stablecoins is shifting from simple supply growth to the underlying economic models and the distribution power of the platforms that hold the assets.

Editor’s Analysis & Impact

The emergence of OpenUSD signals a maturing stablecoin market where the focus is shifting from mere asset issuance to the capture and distribution of reserve yield. For years, issuers like Circle and Tether have enjoyed a lucrative business model driven by interest income on massive dollar reserves. By incentivizing distributors—such as wallets, exchanges, and payment processors—with a share of this yield, OUSD is attempting to commoditize the issuer role. However, the ‘moat’ in the stablecoin industry is not just the technology, but the regulatory compliance and liquidity depth. While OUSD may pressure margins, it faces a steep climb to displace USDC, which is already woven into the fabric of global on-chain settlement. The future of the sector will likely see a bifurcation: regulated, high-liquidity stablecoins for institutional use, and yield-sharing consortium coins for retail and payment-focused ecosystems.

Frequently Asked Questions

Q: How does OpenUSD differ from USDC?

A: The primary difference lies in the economic model. While Circle retains the majority of reserve interest income from USDC, OpenUSD distributes that interest among its 140+ corporate partners.

Q: Does the launch of OpenUSD mean USDC will lose its market dominance?

A: Not necessarily. While OpenUSD challenges the issuer-centric model, USDC maintains significant advantages, including deep liquidity, widespread integration across DeFi and centralized exchanges, and a strong regulatory framework.

AI Disclosure: This article is based on verified data and official reports. Our Team and AI have cross-referenced every financial detail with primary sources to ensure total accuracy.

More from this Category